The financial issues of family planning has become a hot topic, because asking people increasingly start is what the family's financial planning. Then, as financial planning, be true?

Apparently, the problem is in us. Different kinds of people in this world, because apparently all live the dreams and desires for a comfortable and pleasant's Got, and a variety of ideas and ideals, but how many of those who really want to realize their ideas and ideals, was his dream to live or bad? Remember, everything is a price to pay, let us not because it wants faster you need to realize the dream of high seriousness and commitment. Apparently the hardest part is not exactly different plans, but how do I run a plan itself, so our goal is reached.

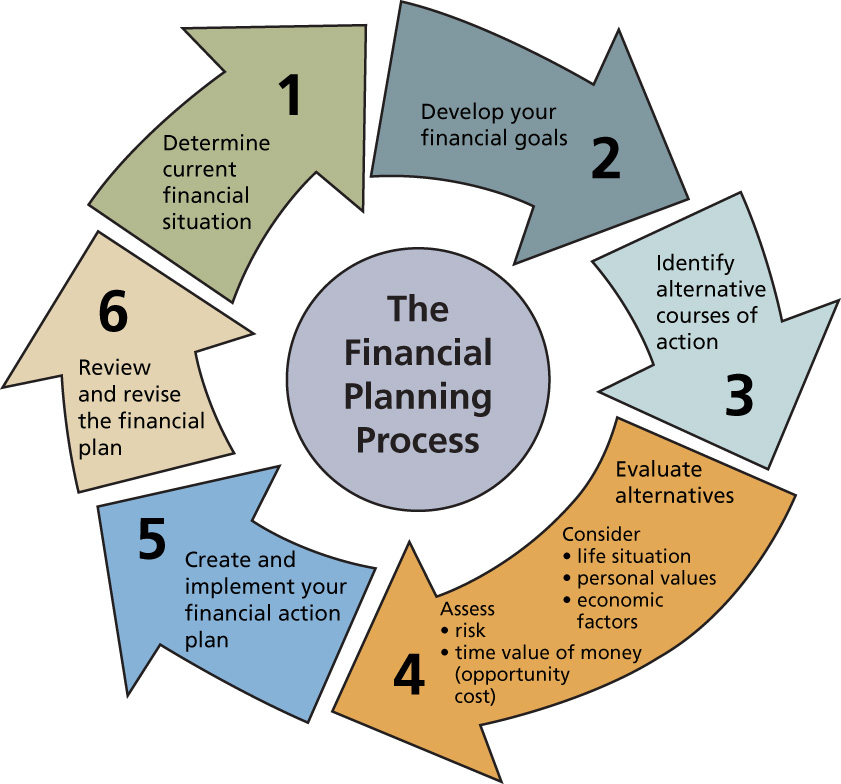

According to me, as you answer the financial question, you can learn, or even if you learn to not have the time and create your own, you can ask financial planners to help set one up for you. But on what? This is a guide or a guide or an integrated set of planning your family's financial planning, and nothing means more than just a book report. The question then, what?

For the success of your financial planning, to the mentality of self-administered, no phone, you can NAPO aka No action .... It .. it .... Therefore we need three main attitudes are: discipline) - 2) Discipline - 3) discipline. It appears that the evolution of a discipline which is not easy to discipline by his lifestyle should be a long time and it is not often easy. Discipline is the realization of a clear obligation. examples of people want to lower blood cholesterol, should modify their behavior and unhealthy lifestyle, it can reduce fatty foods such as discipline seafood, dagingan consumption of meat and more vegetables and fibers. If disciplined, and I certainly have never run this scheme, if my high cholesterol. Just click on "Discipline". A bodybuilder who has always been with rigorous training schedule and eating habits. Very often we can hear the saying that "You are what you eat" or something similar to what the law of sowing and harvesting clearly the law of nature, which can be used. Lo, it is not different in many ways ... You owe your success to accumulate from time to time, so you can make the next jump in success. It is not possible if the people whose lives richly, not want to live not on the priority scale, no savings and investment, and not have a clear financial plan before not even for financial planning at all, more comfortable and convenient in the future. Therefore, we draw a simple lifestyle so that you stand the hard life in future.

Remember that God Mmberkati people who really want to be truly blessed, not people who do not like how it is possible to produce rice fields was, Farmer was not working, if the care membajaknya hoe him occasionally, until the harvest time has arrived. Similarly, life must be treated, we introduce the roles and responsibilities, and God the Creator we see how serious we are and the blessing will certainly be upon us. I hope so.

Apparently, the problem is in us. Different kinds of people in this world, because apparently all live the dreams and desires for a comfortable and pleasant's Got, and a variety of ideas and ideals, but how many of those who really want to realize their ideas and ideals, was his dream to live or bad? Remember, everything is a price to pay, let us not because it wants faster you need to realize the dream of high seriousness and commitment. Apparently the hardest part is not exactly different plans, but how do I run a plan itself, so our goal is reached.

For the success of your financial planning, to the mentality of self-administered, no phone, you can NAPO aka No action .... It .. it .... Therefore we need three main attitudes are: discipline) - 2) Discipline - 3) discipline. It appears that the evolution of a discipline which is not easy to discipline by his lifestyle should be a long time and it is not often easy. Discipline is the realization of a clear obligation. examples of people want to lower blood cholesterol, should modify their behavior and unhealthy lifestyle, it can reduce fatty foods such as discipline seafood, dagingan consumption of meat and more vegetables and fibers. If disciplined, and I certainly have never run this scheme, if my high cholesterol. Just click on "Discipline". A bodybuilder who has always been with rigorous training schedule and eating habits. Very often we can hear the saying that "You are what you eat" or something similar to what the law of sowing and harvesting clearly the law of nature, which can be used. Lo, it is not different in many ways ... You owe your success to accumulate from time to time, so you can make the next jump in success. It is not possible if the people whose lives richly, not want to live not on the priority scale, no savings and investment, and not have a clear financial plan before not even for financial planning at all, more comfortable and convenient in the future. Therefore, we draw a simple lifestyle so that you stand the hard life in future.

Remember that God Mmberkati people who really want to be truly blessed, not people who do not like how it is possible to produce rice fields was, Farmer was not working, if the care membajaknya hoe him occasionally, until the harvest time has arrived. Similarly, life must be treated, we introduce the roles and responsibilities, and God the Creator we see how serious we are and the blessing will certainly be upon us. I hope so.