Too many families are one of the most contentious issues of financial planning, because it seems that the money from equality is not really out of money. It seems that much more money will be spent over what is earned by families. Each family should assume responsibility for finance with effective planning while eliminating the bad technical expenses. One way to increase the affordability of your family is preparing a strategic plan to reduce debt exposure, while strengthening family loans into one loan with lower interest rates. For example, with increasing problems with credit cards is recommended to destroy all your credit cards and keep only one to stay out of debt.

For planning and maintenance of sound finances, a family needs to carry out plans for the money from other savings and reduce the time expenditure. How is your family involved in a viable long-term financial is a great idea. Involve your family in the business of cost control for the better future of money. Try to save electricity, the distinction between needs and wants at the time of purchase, purchase services optimally and other items in bulk to save money. Gain technical costs ensures that your money is not wasted.

Another technique can be used as financial adviser to help with the objectives of the family finances. You do not have to worry about your finances getting out of hand. Financial Advisor responsible for financing the budget to eliminate wasteful spending, reduce high interest payments, and transfer of all liabilities of wealth. But at the same time to participate in professional financial planning advice, you should keep in mind few things.

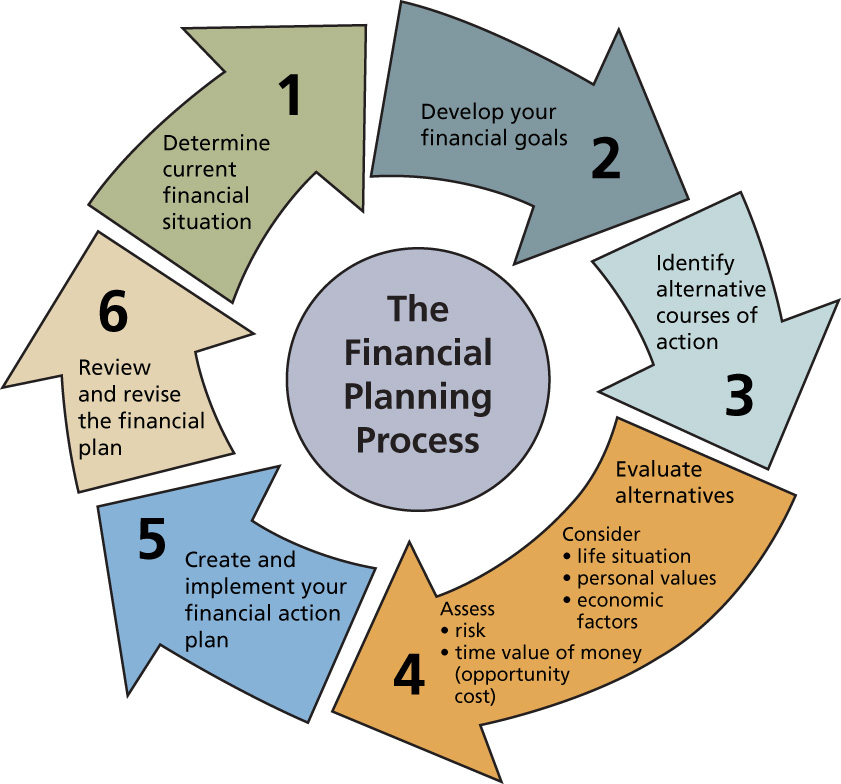

Gather information about the process begins with monetary financial information of the family. Although the appointment of a financial adviser aware of their own assets, liabilities, obligations and liabilities should be collected. It has more stock of financial guarantees. The next step is to identify targets in the short and long term economic family. It may include the level of funds and the income of the family want to achieve different patterns, income security, training, pay, retirement planning and design and other unforeseen events.

Identification of financial problems are an important part of financial advice. Financial adviser gives a helping hand here by comparing the real economic situation allowed monetary goals to develop the best strategies for achieving the objectives. It will take the strengths of the family money and weaknesses, while preparing the financial plan. Adapted plan based on financial needs of the family is designed to achieve all desired goals.

After all the recommendations in the financial plans are agreed, must be applied. All necessary documents are prepared and signed by the client and financial advisor. As the financial plan should be reviewed periodically for updation. In the course of interaction between you and your planner can help monitor progress and achievement of financial plans as they continue their existing investments. Managing your family finances will not be a difficult task with the tips mentioned above.

»» READMORE...

For planning and maintenance of sound finances, a family needs to carry out plans for the money from other savings and reduce the time expenditure. How is your family involved in a viable long-term financial is a great idea. Involve your family in the business of cost control for the better future of money. Try to save electricity, the distinction between needs and wants at the time of purchase, purchase services optimally and other items in bulk to save money. Gain technical costs ensures that your money is not wasted.

Another technique can be used as financial adviser to help with the objectives of the family finances. You do not have to worry about your finances getting out of hand. Financial Advisor responsible for financing the budget to eliminate wasteful spending, reduce high interest payments, and transfer of all liabilities of wealth. But at the same time to participate in professional financial planning advice, you should keep in mind few things.

Gather information about the process begins with monetary financial information of the family. Although the appointment of a financial adviser aware of their own assets, liabilities, obligations and liabilities should be collected. It has more stock of financial guarantees. The next step is to identify targets in the short and long term economic family. It may include the level of funds and the income of the family want to achieve different patterns, income security, training, pay, retirement planning and design and other unforeseen events.

Identification of financial problems are an important part of financial advice. Financial adviser gives a helping hand here by comparing the real economic situation allowed monetary goals to develop the best strategies for achieving the objectives. It will take the strengths of the family money and weaknesses, while preparing the financial plan. Adapted plan based on financial needs of the family is designed to achieve all desired goals.

After all the recommendations in the financial plans are agreed, must be applied. All necessary documents are prepared and signed by the client and financial advisor. As the financial plan should be reviewed periodically for updation. In the course of interaction between you and your planner can help monitor progress and achievement of financial plans as they continue their existing investments. Managing your family finances will not be a difficult task with the tips mentioned above.